3 Common Challenges Faced by CEOs when Choosing a Co-Founder

- #1: Too Many Co-founders

- #2: The Equity Split

- #3: Founder Drama

This is our second post on co-founders. As we’ve said in our previous post, picking the right or wrong co-founders will shape your entire startup journey.

Here. we outline the common challenges of picking a co-founder.

Founder challenge #1: Too many co-founders

Some startups fall prey to the too-many-founders syndrome. This can create both short-term and long-term problems. There’s a clear right and wrong here: fewer co-founders is better than more.

In the early stages of an enterprise startup, co-founders make numerous major directional decisions that impact the fate of the startup. Having too many co-founders complicates decision-making. Too many co-founders makes determining equity ownership for founders more complex. Too many co-founders can drive a company to do organizational gymnastics to place people who have a co-founder title in meaningful roles. Too many co-founders often means some founders have a lighter workload than others, which can lead to resentment among the other founders and the rest of the team. This, in turn, can lead to founder instability and conflict over equity ownership.

The decision to add a co-founder is a serious decision. Before adding a co-founder, ask these questions: Does the person have founder fit? If so, does the person bring a needed capability to the startup that justifies adding a founder right now? Could an existing founder or key advisers do it instead, at least for now? If the answer to that last question is yes, you’ll probably be better off not making that person a co-founder, and instead hiring them (or somebody else) later as an executive.

Founder challenge #2: The equity split

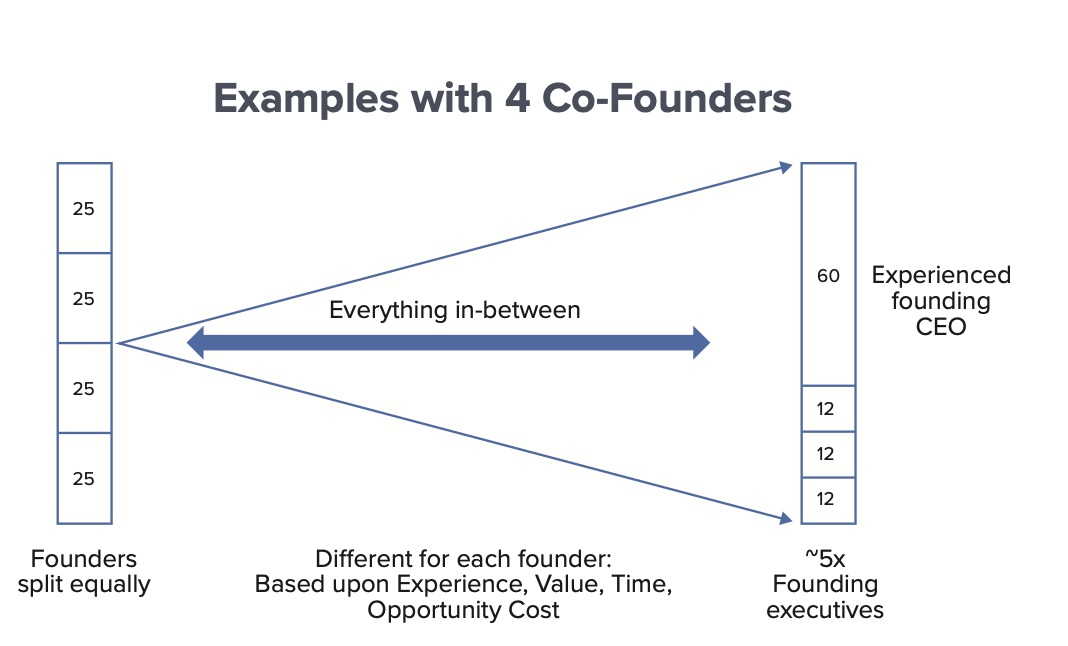

How do founders split equity? This is a financial question—and an emotional one. Every situation is different, and no amount of data and comparables will get you past that. Founders will have different views of fairness, of their contribution to the Founding Idea, of the value they bring, of prior relationships, of timing, alternatives, and so on. It’s difficult to capture those elements all at once. The resolution of this question is specific to each founding team with many outcomes along a possible spectrum. (See the following chart.)

On the left end of the spectrum, every founder is the same, and the founders split equally. On the right end of the spectrum, one founder, usually a proven founder-CEO, gets the largest share, with other founders divvying up the remainder.

At the right end of the spectrum, a common ratio for the equity given to an executive and the CEO is 1:5, which can be less if the founder is not likely to be a long-term executive.

The hard part is that most founder situations fall somewhere in between. Different founders bring different value and experience to a startup. Different founders forego different opportunities to join the founding team. All of that has to be factored in. And it has to be done in a way that makes sense to everybody. In some cases, a useful tool to bridge gaps is to create future equity grants for founders that are tied to specific business outcomes, such as product delivery or customer targets. But the bottom line is that determining founder equity is always tricky—and very personal.

Tae Hea: “The founder-split decision has a surprisingly long half-life inside a company. In several companies, co- founders raised the ‘unfairness’ of the original split many years after the company’s founding, and after many refresh grants. I’ve learned that the founder equity split is more than economics. For the founders, it conveys a message about personal value.”

Founder challenge #3: Founder drama

For co-founders, embarking on a start-up is like getting married, often without much dating. The challenge, unfortunately, is that sometimes co-founders only later realize they don’t work well together, often resulting in bitter founder drama. Employees are forced to take sides. Decisions are paralyzed. Culture is damaged. It’s like a divorce that creates collateral damage to the company, employees, and investors. Some common reasons for founder drama:

- The founders don’t agree on the vision, direction, values, or culture. Even the smallest disagreements are magnified in the very high-stress world of an early-stage startup.

- It’s not clear who the CEO is. Early founder leadership roles are fluid. Sometimes a non-CEO founder raised most of the early capital. But in the end, there needs to be one CEO who can make final decisions. Lack of clarity or latent resentment about who is CEO creates toxic politics.

- One co-founder is perceived as not contributing or working to the same level as the other co-founders. Everybody has to carry their weight.

- The co-founders disagree about equity allocations. After raising capital and allocating equity for employees, the remaining equity is sometimes not enough to satisfy every founder. This problem is magnified if there are disagreements on the prior three reasons.

Founder drama can exasperate employees and investors and make them give up. Founder drama can quickly kill a startup. Some companies can survive founder drama if they have CEOs and boards who act quickly and decisively in response, but the best approach to founder drama is to prevent it from happening in the first place. That means thinking hard before making somebody a co-founder. Carefully consider what it will be like to work with that founder candidate, and the candidate’s fit with the ground rules on vision, values, culture, equity, and lines of authority.

We’re serialising our first book Survival to Thrival: The Company Journey online to make the full content of the book available for free for all enterprise entrepreneurs. This is our fourth extract, taken from Chapter 1.

Subscribe to our occasional newsletter to make sure you don’t miss when we publish some key content.